#Woke. Impoverished communities rallied together in the wake of a disappointing election cycle. For me, and many others who have come into contact with this country's social safety net, #woke was a defining moment where we told the world that "we are acknowledging the fact that our government - and middle class white America for that matter - doesn't care for us." Or at least that they don't know how to care for us.

There are a bunch of people struggling in the middle class who feel that the majority of low-income folks are "taking advantage of the system". And there are a lot of people in the welfare system who see the middle class and think "you have so much money... stop complaining." That being said, I have traversed both of these income levels and both socio-economic situations are fraught with struggling. However, the very low income earners who must utilize public housing, and other types of public assistance are at a severe disadvantage when it comes to making positive changes that contribute to wealth-creation.

The path of increasing income to get out of debt, save money, and build wealth is blocked off for families who take advantage of SSI and low income housing. In our classes, we teach people to accelerate paying off debt and to save three to six months worth of household expenses for emergencies. One way to do this is to work additional hours or find a part time gig. This is fine for someone who is not using the social safety net. However, for someone utilizing low-income assistance, their living expenses increase and benefits decrease as their income increases - a real squeeze.

I have experienced this first hand. When I was in college, I had a simple workstudy job. I didn't earn more than $10 per hour before I got a call from back home. It was my older brother, who told me the NY housing authority said I was earning too much income and they were going to raise the rent. He went on to say, I could either make less money (quit my job), or he would have to remove me from the apartment lease (get kicked out). I was 17 years old, and here I was; my first real full time job and a choice... I could either quit my job and continue to live at home, or leave home and take my chances. I chose the latter. This choice was worth hundreds of thousands - if not millions - of dollars at the very least. And it doesn't include the economic impact on my family for generations to come. But there are many who don't make that decision because of the immense pressure to align to the status quo. If my entire family - aunts, uncles, cousins - all live in these tenement project high-rises, why shouldn't I limit my work hours and take the advice to go and apply for the same benefits my family has?

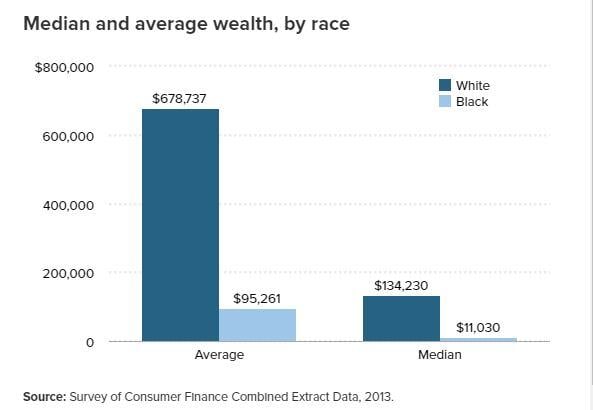

The reason is below. Let's look at the staggering statistics about wealth inequality. The chart below shows the huge disparity in average and mean wealth between blacks and whites.

It is my theory, that the huge disparity between the wealth of this country's minority population and their majority counterpart is due to the fact that African Americans and Hispanics make up only 13% and 17% of the population and yet account for the vast majority of people utilizing public housing.

How does public housing affect median wealth?

1. There are strict income requirements: If you remember from my earlier example, I simply had a low-paying job in college that was making me less than $10 per hour and my family essentially had to kick me out of the apartment to avoid a rent hike. With limits on your income, you can't build much wealth.

2. There are strict asset requirements: You have to declare any assets, including any savings accounts. Generally, if you have savings, the interest that you earn is counted towards your income limit. And worse, is that most people in low income housing are utilizing social security insurance (SSI) benefits, which allow you to only have up to $2,000 in assets before you are ineligible. And don't forget, the asset limit is supposed to include anything that can be traded for cash. Things like cars and furniture, but most won't report that because it's nearly impossible in this day and age to have less than $2,000 worth of 'stuff'. So in many cases you essentially cannot own anything.

I was counseling a friend who fell on some hard times and was on social security disability in a rent subsidized apartment for a while. After he recovered, he wanted to rejoin the workforce and he got a job. I gave him the standard advice... Stop using any credit cards, save $1000 in the bank for emergencies, start paying down the high interest debt, and then continue saving for emergencies, and start saving into a Roth IRA. He quickly got a job. He did well and his boss wanted to give him more hours, but he had to decline because the public housing authority would raise his rent, and his SSDI would lapse before he got health insurance from the employer. It upset and hurt me deeply because I felt like my money advice was just out of his reach... This is the community I grew up with and want to help dearly. So I did what scientists do... I did as much research as i could on the subject of climbing out of the society safety net without getting caught in a snare.

I am developing this list continually, and if you subscribe, you'll be first to know when there are updates. But here is what I've found so far. I tried to make a plan that was as general as possible so the most people can access it. So please, make sure to read the rules that apply to your specific situation so you don't get into trouble navigating the waters as you take control of your life and begin to build your wealth. In our 5-week financial bootcamp, we give our community 5 financial peaks to conquer. I've modified this for the murky waters of separating ourselves from the public assistance safety net.

1. Create a budget from now until the day you stop breathing. You can never make too much or too little to not have a budget. Even if your income is $100 per month, you need a written budget. We can show you how to do it. The earlier you can learn this skill, the more likely you are to succeed.

2. Decide whether or not you want to get off of public assistance. The social safety nets are in place for a reason. About a third of people using public housing are over 60 years old and might need the assistance for the remainder of their lives for any number of reasons. About 20 percent are disabled and may not be able to sustain full-time careers for medical reasons. Three quarters of those in public housing are headed by a single female and their circumstances may not allow them to work full time. Everyone's situation is different and for some, it may simply not be possible to go back into the workforce. If you think deeply and decide that your best choice is to continue with your benefits, there's no shame in it as long as you've made a mature decision to do so.

3. Determine the cost of living where you live (or where you will live). If you're living in public housing, it's possible that your rent is well below what the median rents are in the area that you live in. For example, a person in New York City might have a rent of $1500 for a 1 bedroom 300 square foot apartment. Meanwhile, a rent-subsidized apartment may have a rent of half that or less depending on the individual's income. If you've never had a non subsidized apartment or if it's been a while since you've rented outside of public housing, the initial sticker shock of rent can be discouraging, especially for high-cost of living areas like NYC. But it's important to know the numbers. The good book says 'don't build a tower without first counting the cost'. You don't want to start making money, lose your benefits, and find out you can't afford to live after the fact. A good exercise is to build a second budget that shows how much your new expenses would be if you didn't have your benefits anymore.

4. Gather mental assets - marketable skills. Since you're limited on the value of monetary assets you can have while receiving benefits, you need to increase your earnings potential by massively increasing your skill-sets. If you previously had a skill that you plan to use, make sure to renew your certifications that you need to work and make sure there is still demand for your skill set. Alternatively, you can research careers that interest you that would also provide, on average, enough income to sustain an average household in your area (you researched this in step 3). Websites like Glassdoor are great for doing research on the average salaries for different fields and even specific jobs at specific companies. Once you've found something you like, look for need-based scholarships and grants to pay for education. Online courses at local community colleges are generally inexpensive enough to be covered by Federal grants. Try to stay away from the student loans as much as possible, especially the unsubsidized loans. If you do take out loans, you have to add the repayment to your expenses that you calculated in step 3. Spend as much time as you need acquiring the skills that can lead to careers that will cover the cost of living in your area. The goal is to build a particular set of skills so that you can start immediately applying for professional level jobs, or entry-level jobs with a higher median salary than the median cost of living in the area. The idea is not to rush to get out... take your time and take advantage of the free/ low-cost resources at your disposal to massively increase your earning potential as high as you can before you make the leap. Take career-building classes, get an associates, bachelor's, and a master's degree while those resources are still at your disposal. Apprenticeship programs for the skilled trades are good too, but be mindful that some of these programs pay you while you learn, so keep an eye on the income limitations for your situation.

5. When you are within a few months of reaching your degree or certification, begin job-hunting. There is lots of advice on job-hunting, but one of the best ways to score an interview is to tailor your resume directly to the employer's ad. Being as truthful as you can, your resume should contain a mirror of the job description. If the job asks for someone who can program Java and is good at managing projects, the section before your job experience and education should have a "skills" section that says: "Skills: Java programming, Project management, ..., etc.". It allows potential employers to quickly glance at your resume and see you're abundantly qualified instead of having to read the entire document to determine your eligibility for the job. When you've gotten an offer that you can live off of, pull the trigger.

6. Discourage the youth from utilizing these programs designed for the poor, except as a very last resort. If you are a parent utilizing these assistance programs, teach your kids to budget. Let them budget with you. Teach them about debt, saving, IRAs and home ownership. The youth need people to model a wealthy mindset and healthy attitudes around money and you don't need to be wealthy to instill that mindset. If you decided that you yourself cannot leave the projects, make sure you become a beacon that allows your family tree to grow in a new direction. Teach your friends and neighbors how to build wealth, save and how to avoid the traps that cause poor people to fall into intergenerational poverty.

Now back to #woke....

We saw a completely distasteful and embarrassing election cycle in 2016. Our choices were loathsome (or at least the news made it seem that way). On one hand we had sexist, racist, and every other "-ist"... And the other was a candidate who could not hold a candle to her predecessor - in our eyes anyway. We watched, embarrassed, as both tried to vie for the "Black Vote". Neither connected with the black and hispanic community, who are using these public assistance programs at astronomically higher rates than their majority counterparts. As a result, many just didn't come out to vote and the next morning... Riots. Oddly enough, these riots were mostly made up of middle class students at prestigious colleges... which was a bit strange to see. You know, privileged middle class kids breaking windows and setting trash cans on fire. I'm not saying whether it was right or wrong... it was just strange to see personally. By and large, the minority communities were simply disappointed... again. I found myself strolling through memory lane at past presidents and how they tried to gain the trust of minorities, while failing to understand the culture.

Bill Clinton seemed to come close when he appeared on the Arsenio Hall show back in 1992. The African American community was floored - my 6-year old self included. The fact that this guy from Arkansas... appeared on the show, and then was ballsy enough to get down on the sax and jam with the band - sunglasses and all. I remember my 6-year old self, confusing Arkansas for Kansas, and confusing Bill Clinton for Clark Kent. Our Superman had come!

Clinton was doing fine in the eyes of the public until he faded into the sunset amidst the biggest sex scandal in U.S. Presidential history. Despite his economic achievements on paper, minorities still floundered at the bottom of the economy, but we weren't #woke yet.

And then there was GW Bush. He also tried to vie for the black vote by acknowledging the history of this country and empathizing with the Black community while he was campaigning in 2000. That might have been even more gutsy than Clinton's sax performance. You can cut the tension with a knife...

In any case, minorities didn't expect much from GW... We got a couple of wars and a start to the biggest financial meltdown since the Great Depression. While this all happened, minorities continued to flounder at the bottom of the economy. And then there was hope.